Alexandra Miles Senior DC fund manager and E2W member - Why it matters?

katie.robertson / 24 Nov 2023

Pensions serve as a useful lens through which to assess the result of a culmination of life’s inequalities.

“The goal is to turn data into information, and information into insight”[1]

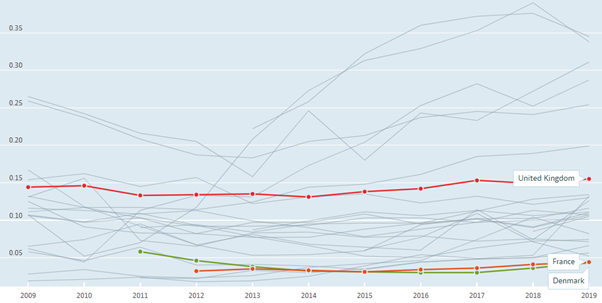

Let’s start with the data, what does this tell us?…Houston we have a problem.

Poverty rate, European union, 66-year-olds and older, Ratio, 2009-2019[2]

The poverty rate shown in the chart above is calculated by the Organisation for Economic Co-operation and Development (OECD) as the ratio of the number of people (in a given age group) whose income falls below the poverty line; taken as half the median household income of the total population. The UK stands out on the chart above for its relatively high poverty rate, with only the Baltic states and some Balkan region countries with higher rates of poverty for those aged 66 and over. Adding to this we also know that there are pockets within society that are more at risk than others, two examples being women and those from minority ethnic communities.

“For the strength of the pack is the wolf, and the strength of the wolf is the pack”[3]

There has been growing concern across the pensions industry about retirement adequacy and known inequalities in current retirement savings for some time. We can all do better, but a few passionate individuals working within the industry were keen to use their collective experiences and expertise to make a real difference, shifting the narrative over time, hence the launch of the Pensions Equity Group (PEG) in late May this year.

We’ve organised ourselves into four sub-groups: Data and Research, Government and Policy, Communications and Awareness, and Product changes, in order to make quicker progress, working together to advance known areas of interest and in so doing move the conversation on.

Building a comprehensive picture of an individual’s retirement savings, but at a population level is incredibly difficult to do, something our group hopes to be able to help with.

In the UK we have three pillars of retirement savings, common across many countries – state pension, workplace pension and private pensions. Our group will be looking across all three, establishing where the broader pensions adequacy concerns lie in aggregate, and what can be done to solve these moving forwards.

As the average individual is expected to accrue workplace pension savings across on average 11 different employers by the time, they retire[4], building a holistic picture of someone’s retirement savings is hard to do, something the Pensions Dashboard when up-and-running should help address.

Greater communication and engagement with individual members is one strand, but will be a slow burn. Other key stakeholders such as employers and trustees, providers and the Government need to play their part in order for the right change to happen, and quickly.

“Doing the right thing is more important than doing the thing right”[5]

Exploring some of the hurdles that people face when wanting to save for their retirement, through assimilating proper data and research, from a number of different fields and experts is key to building a case for change – lots of the information already exists, the power now lies in using this to build an argument as to why the status quo must shift. The implications of the decisions that an individual makes throughout their life on their accumulated retirement savings has an impact not just for them but society at large.

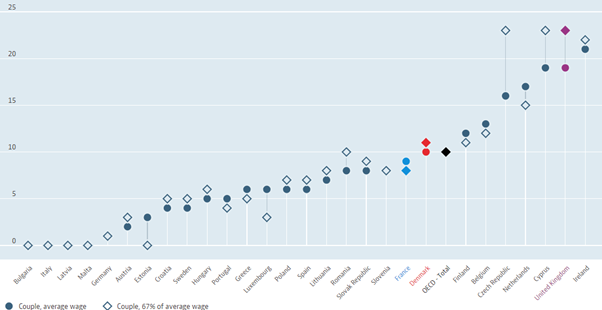

Picking just one of these and one that is often used in discussions around the main factors contributing to a gender pensions gap - current childcare costs in the UK, the chart below nicely illustrates the issue at hand. Due to the cost, many families don’t have a choice when it comes to deciding whether or not to return to the workforce after having children. As a result, these individuals lose the chance to contribute to a workplace pension, and the UK at large loses their contribution to the UK economy, something that is needed so desperately.

Net childcare costs, assuming two children aged 2 and 3 using full-time centre-based childcare, 2022 or latest available[6]

Other areas of focus that spring to mind would be the changing landscape for ongoing housing costs, and implications of the industry sector and type of work you do on the affordability and accumulation of your retirement provision.

It is often said that in a traditional household setup, resources will be pooled so everyone should be OK and the fact that one might take a financial hit during their working lifetime shouldn’t matter when retirement looms. This is lazy thinking. Life almost never works out as we plan. We should be striving to make sure that all individuals are financially secure, regardless of their life path and the personal partnerships they have formed along it.

“We are kept from our goals, not by obstacles, but by a clearer path to a lesser goal”[7]

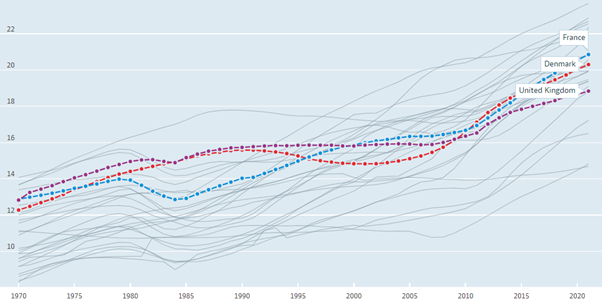

There are huge shifts going on at a societal level in the UK, the shift from DB to DC workplace savings, and with it the overall responsibility for a reasonable retirement transitioning from employer to employee. There are also the large demographic changes accelerating quite quickly for many countries including the UK, with the rise of an aging population the very idea of retirement as we know it is up for challenge, requiring some new thinking, and that’s where the Pensions Equity Group comes in…

Elderly population, total % of population, 1970-2021[8]

References:

[1] Carly Fiorina, former executive, president, and chair of Hewlett-Packard Co.

[2] https://data.oecd.org/inequality/poverty-rate.htm#indicator-chart

[3] Rudyard Kipling

[4] https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/214585/cp-oct10-full-document.pdf

[5] Peter Drucker

[6] https://data.oecd.org/benwage/net-childcare-costs.htm#indicator-chart

[7] Robert Brault

[8] https://data.oecd.org/pop/elderly-population.htm

Back to blog